Americký ministr financí Scott Bessent ve čtvrtek požádal Kongres, aby v souladu s dohodou s ostatními zeměmi zrušil článek 899 z návrhu rozpočtu.

Toto ustanovení, které je v současné době součástí Trumpova zákona o snížení daní a výdajích, by americkému prezidentovi dalo pravomoc přijmout odvetná opatření proti zemím, které uvalí na velké americké technologické společnosti zvláštní daně z digitálních služeb, které budou považovány za nespravedlivé.

„Po měsících produktivního dialogu s ostatními zeměmi o globální daňové dohodě OECD oznámíme společné porozumění zemí G7, které hájí americké zájmy,“ uvedl Bessent v příspěvku na X.

Žádost přichází po diskusích s mezinárodními partnery o globálním daňovém rámci Organizace pro hospodářskou spolupráci a rozvoj.

Yesterday, US equity indices finished mixed. The S&P 500 rose by 0.58%, the Nasdaq 100 jumped by 1.20%, while the Dow Jones Industrial Average fell by 0.14%.

All eyes were on the Trump–Xi meeting in Beijing, which ended without any dramatic breakthroughs, and markets reacted accordingly. After a record rally the previous day, global equity indices traded around their recent highs, but the summit did not deliver new catalysts to push futures significantly higher.

Trump described the talks as "excellent" and spoke of a "fantastic future" for both countries. Xi Jinping called for partnership over rivalry. The business delegation set a positive tone: Nvidia's Jensen Huang and Tesla's Elon Musk accompanied the president, and Huang also called the meetings "excellent." China pledged to open its market more to US business. A concrete outcome was US approval to sell high-end H200 chips to ten Chinese firms, including Alibaba and Tencent — arguably the most tangible agreement from the visit.

The upbeat mood was tempered by the Taiwan issue. Xi directly warned Trump about the risk of conflict if the island situation is "mismanaged," and markets registered the signal. The Taiwan question revived discussion of a geopolitical risk premium — the very premium investors had been overlooking amid recent optimism.

China's market reacted to the summit outcome with losses in a classic "buy the rumor, sell the fact" reaction: the CSI 300 fell by 1.7%, led by weakness in the tech sector. Offshore yuan, however, strengthened for an 11th consecutive day, marking its longest run since 2017.

Almost unnoticed amid the summit was an important domestic development in the US: the Senate narrowly confirmed Kevin Warsh as Fed chair, one of the most controversial leadership changes at the central bank in decades. The appointment comes at an inconvenient time of rising inflationary pressures, and the new Fed head will face difficult decisions from day one.

April producer prices rose by 6.0% year-on-year, the strongest pace since 2022 and above consensus. Energy, lifted by the war and higher shipping costs, was the main contributor. That data briefly cooled the equity rally, which soon resumed.

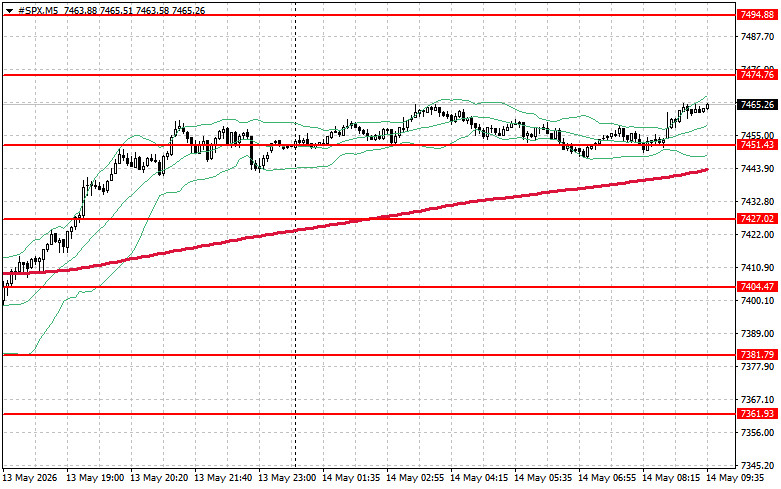

Technically, the S&P 500 analysis suggests that the immediate task for buyers is to overcome the resistance level of $7,474. That would confirm further upside momentum and open the path toward $7,494. Maintaining control above $7,518 would further cement buyers' advantage. On the downside, buyers need to defend the $7,451 area. A break below that level would likely push the index back to $7,427 and open the way to $7,404.